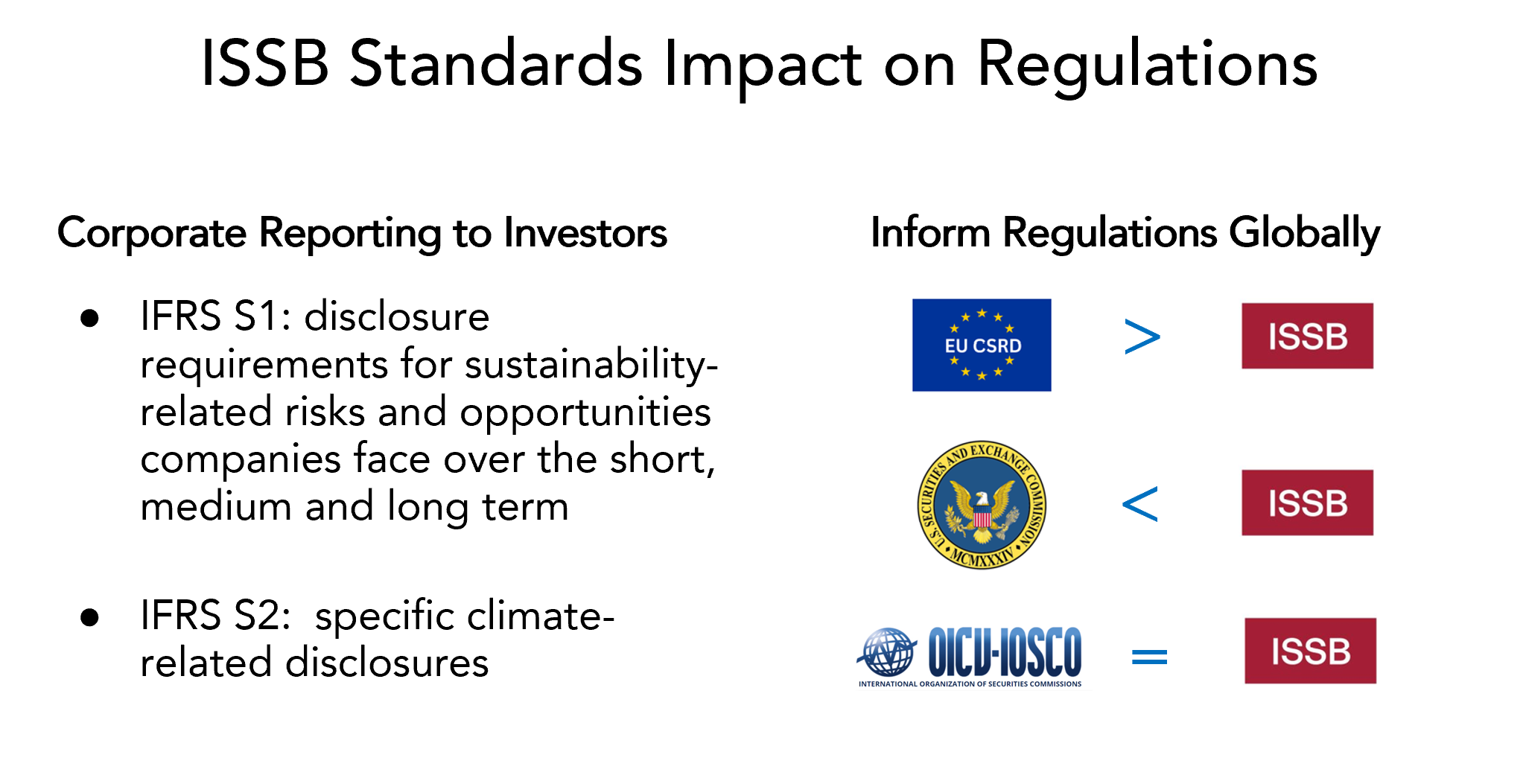

The International Sustainability Board published their inaugural standards detailing the ESG information investors require of companies. Endorsed by IOSCO, the standards are already informing the regulations which will require companies to comply.

The International Sustainability Standards Board has set the new standard for sustainability. Literally. They have spelled out the responsibility of firms to disclose environmental, social, and governance (also known as ESG) information to their investors—whether owners or lenders—irrespective of whether a firm is publicly or privately owned. Those standards—known as IFRS S1 and IFRS 2—are effective January 1, 2024 are already informing regulations that will require companies to use them.

Standards Converge with ISSB

IFRS S1 is the overarching sustainability standard that sets the stage. IFRS S2 is the sustainability standard that specifically addresses climate change. They are designed to:

-

Meet the needs of investors (owners or lenders) in the ‘General Purpose’ Financial Statements, and

-

Disclose sustainability- (S1) and climate- (S2) related risks and opportunities which ‘could reasonably be expected to affect the entity’s prospects’ (aka financial performance)

These standards are based on the foundational work of people who have been working in this space for decades, starting with the GRI (Global Reporting Initiative), founded by Ceres and UNEP in 1997. Originally developed through a coalition of investors and environmentalists led by Joan Bavaria to find a better way of doing business in the wake of the Exxon Valdez disaster, the GRI standards today meet the needs of multiple stakeholders. They are the most widely used sustainability reporting standards globally.

However, the GRI did not always meet the specific needs of investors, and over time additional standards emerged, including SASB (Sustainability Accounting Standards Board), IR (Integrated Reporting), TCFD (the Task Force for Climate-related Financial Disclosure of the Financial Stability Board), and CDSB (Climate Disclosure Standards Board of the Climate Disclosure Project, now known as CDP).

The ISSB has combined this alphabet ‘soup’ into cohesive standards, in a remarkable display of collaboration and leadership, which they acknowledge complement the GRI.

The Essentials of the ISSB Standards

The standards require information structured around 4 thematic areas that represent the core elements of how companies operate: governance, strategy, risk management, and metrics and targets. That’s a direct result of the TCFD recommendations, published in 2017 (and already used by a number of leading firms).

Governance answers the question: ‘Who’s responsible?’ It’s both at least a representation of ownership (board) and senior management. It also includes the processes for governance and an explicit requirement to assess skills and capabilities and build necessary skill development into the strategy.

Strategy answers the question: ‘What are you doing (and why)?’ It’s central to the firm—not a ‘special effort’ led by a group that is ‘off to the side.’ The standards are very broad—they include business model and value chain and the processes by which strategic decisions are made. In the climate-related standard (S2), it specifically calls for resiliency.

Risk Management answers the question: ‘What are the (most important) risks and opportunities?’ And ‘How do they connect with your business performance?’ This standard requires more than a simple list. It requires that firms ‘connect the dots’ between the sustainability risks and opportunities and the effects on the entity’s financial position.

In S1, the standard allows for firms to determine their own overall sustainability risks, but the ISSB strongly recommends the guidance provided by SASB for industries (they have developed this for 77 industries) and CDSB, which spells out water and biodiversity risks.

For climate-related risks (S2), there are both physical risks and business transition risks. The former seeks to understand the implications of physical risks—e.g., flooding, drought, extreme heat, increasingly volatile weather, etc.—on the business. For business transition risks, the standard recognizes that businesses which rely on ‘high carbon’ (e.g., fossil fuels) will suffer with a transition to a lower carbon economy, if not appropriately addressed. In addition, the standard specifically requires firms to create and share scenarios regarding these risks and opportunities.

Metrics and Targets answers the question: ‘How are you performing against sustainability-related risks and opportunities (including progress toward any targets)?’ SASB, CDSB, and GRI all provide guidance for specific metrics that firms may consider using to meet the requirements for S1, but the climate-related standard (S2) specifically calls out for carbon dioxide (CO2) equivalents of the 7 greenhouse gases, as defined by the Greenhouse Gas Protocol (GHG Protocol). It requires reporting for all 3 ‘scopes’:

-

Scope 1 includes direct emissions from operations owned or controlled by the company;

-

Scope 2 includes emissions from the generation of purchased electricity, steam, heating, or cooling used by the company (generally, these are from utilities);

-

Scope 3 includes the indirect emissions that occur in the value chain of the company, both upstream and downstream, which means it includes both supply chain and any associated emissions with the life of a firm’s product (or service) throughout its use and end-of-life.

All of this must be reported within the context of ‘general purpose’ financial reports (the ones that are made available to investors).

Mike Wallace, Persefoni’s Chief Decarbonization Officer, has a great insight: “Everyone is someone’s Scope 3.” So even if you aren’t required to track GHG by your investors or regulators, it’s highly likely your customers will be, and they will be coming to you for the information to report their Scope 3 emissions.

The standards become effective for reporting January 1, 2024, with transition time built in. The initial demand will likely come first from investors and customers who will require the information, but increasingly, you can expect ISSB standards will also inform regulations around the world.

The International Organization of Securities Commissions—also known as IOSCO—has already endorsed the standards. The ISSB has also worked closely with American, European, Japanese, and Chinese officials to develop its rules as a global baseline and work on interoperability between jurisdictions, but it won’t be perfect. For example, in the US, the still-to-be-finalized Securities and Exchange Commission rules are expected to be a lighter touch than the ISSB (IFRS S1, IFRS S2) standards. The EU Sustainability Reporting Standards, published July 31, 2023, will require more. They do require companies to provide information for investors to understand the sustainability impact of the companies in which they invest, as articulated by the ISSB, but they also require more disclosure, particularly for stakeholders beyond investors (with a specific acknowledgement to the GRI).

WholeWorks Webinar Recording Available

This post is based on the WholeWorks Webinar ‘ISSB: Setting the New Standard for Sustainability,” presented on August 2, 2023. The link to the full recording is here: <link> and includes practical advice to address the new, global requirements. The webinar also gave an overview of a method for developing clear connections to ESG-related risks and opportunities to create and/or preserve value via a Sustainable Value Creation Map. There with more information <here> for the map, including a detailed white paper on the application for readers to apply to their own firms.

WholeWorks offers a short online course for ESG Fundamentals and a longer, simulation-based professional certification course Strategic ESG: Creating Sustainable Value for leaders and professionals who want to accelerate their ability—and the ability of their organizations—to meet the new standard for sustainable business.

P.S. A Word on Auditing

One of the top questions in the webinar’s Q & A session was based on the ‘audit-ability’ of the new standards.

And almost like they were listening in, the International Auditing and Assurance Standards Board (IAASB) published their proposal August 7 regarding a sustainability assurance standard. As David Carlin, Head of Climate Risk and TCFD, UNEP Finance Initiative, points out, ‘External assurance plays a key role in enhancing trust and confidence in financial reporting. It can do the same for sustainability reporting.’ The proposed standard will apply to sustainability information reported across any ESG topic and prepared under multiple frameworks, including ISSB. It’s open for consultation now, until December 1, 2023. IAASB welcomes comments <here>.

This article and imagery was originally published on the WholeWorks website and is re-published here with permission.

About the Author:

Laura Asiala, MSOD

Laura Asiala is the Chief Sustainability Officer of WholeWorks, LLC and the Lead Facilitator for ‘Strategic ESG: Creating Sustainable Value’ Professional Certification Program—in which experienced professionals and leaders accelerate their ability to integrate ESG issues across their companies, creating value and transforming a traditional business to sustainable, via a realistic team simulation. She also curates and edits ‘WholeWorks Connects,’ a publication amplifying the work of leaders in the field of sustainability, including alumni of WholeWorks programs.

CGLR’s business and sustainability network programming is supported by the Fred A. and Barbara M. Erb Family Foundation.

![]()